AS WE CLOSE THE BOOKS ON 2025 and think about the opportunities of 2026, it is important to look back and reflect. Last year we said "Artificial intelligence (AI) has shown up in a big way." This year, some might say that AI has become an overly enthusiastic, slightly awkward eyecare intern. Maybe next year it will come of age. Last year, we said there would be “uncertainty and optimism for the economy.” The Chicago Board Options Exchange’s Volatility Index (VIX) is a measure of S&P 500 stock index volatility. As of this writing, the VIX is 19 (near normal) compared to 16 (normal) 1 year ago. Yes, there are uncertainties ahead, but we do have much to look forward to in 2026 and beyond.

Opportunities will continue to appear in ocular surface disease and myopia control. And a significant event happened in the United States in 2025—the approval of the first spectacle lens for myopia control. This milestone has the potential to alter the standard of care when working with kids and teens, and may have a potential impact on contact lens fitting. For these reasons, we have named it the 2025 Contact Lens Event of the Year (see more on page 1).

Overview of General Market Trends (Contributed by Jeff Johnson, OD, CFA, managing director, senior research analyst)

After 4 straight years of growing above 4% to 6% year over year (y/y) historical averages, growth across the $12 billion global contact lens market came back down to Earth in 2025. Data obtained from Baird suggests that through the first 9 months of 2025, the global soft contact lens market is on track to grow roughly 4% y/y, down from 7% growth in 2024 and 3-year average growth of just greater than 8% during 2022-2024.

Several factors contributed to this slower growth in 2025, most notably the macroeconomic uncertainty in the United States and globally. In the United States, manufacturer price increases that spiked in the early post-COVID period to a nearly mid-single-digit tailwind fell back to the low single digits, with customer rebate activity also picking up slightly. Select manufacturers began offering full rebate opportunities to customers purchasing a 6-month supply of lenses instead of a 12-month supply, a change that could help bolster 2026 growth as some of those wearers come back to the market sooner than they might have otherwise. But in 2025, this created modest customer purchasing headwinds.

A US contact lens survey that Baird published in early November1 found that in addition to customers being less willing to purchase an annual supply of lenses in a single transaction, established contact lens wearers have been less willing to trade up from frequent replacement to daily disposable lenses in recent months.

Despite the slower 2025 market growth, Baird analysts remain confident that there are reasons for optimism moving into 2026 and beyond. First, Baird’s recent survey suggests that new contact lens wearers remain willing to move straight into daily disposables and specialty lenses, including torics and multifocals. Second, Baird’s survey shows that eyecare practitioners remain bullish on future penetration rates for dailies and for specialty lenses, with penetration of daily silicone hydrogel (SiHy) lenses still expected to increase 5% to 6% over the next 1-2 years and penetration for toric and multifocal lenses also expected to increase a few points over the same period.

New product innovation and manufacturing capacity expansion also continued across all major manufacturers in 2025, which Baird believes should set the stage for improving market growth next year, especially if interest rates continue to move lower and help consumer confidence and consumer spending trends pick up after a mid-year fall-off in 2025. In addition, as uptake of dailies and even daily torics and multifocals rebounds, Baird believes global contact lens market growth should get back to the mid to upper end of that 4%-6% historical range by early to mid-2026.

Current Practice Trends

Contact Lens Spectrum also conducts market research, asking readers about their practice trends and patterns both generally and as they relate specifically to contact lenses. We have conducted this market research for many years, which allows for some longer-term and longitudinal analyses. The questions cover a variety of topics, including characteristics of the patient base of a practice, business and financial aspects of a practice, fitting and prescribing trends, and care solution trends. This year, 26 North American respondents completed most of the survey.

In proceeding ahead in discussing trends and observations about the contact lens field, we will draw on information provided through this market research, in addition to other sources. It is important to note that the readers of Contact Lens Spectrum likely reflect stronger focus on specialty lenses in their practices compared with other data sources.

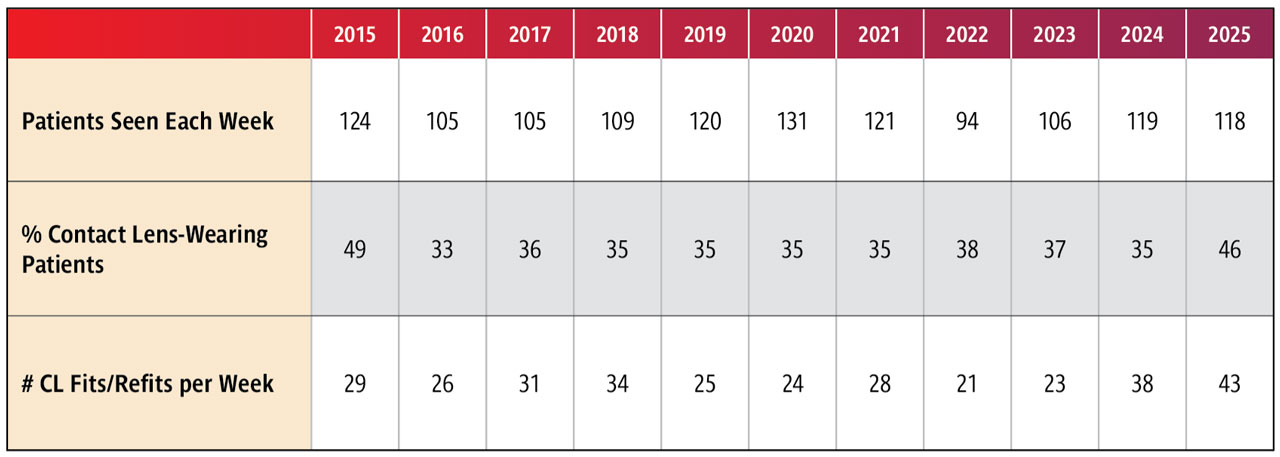

Practice and Business Trends: Table 1 summarizes trends in practice and business characteristics between 2014 and 2024. Most of our respondents were optometrists, followed by ophthalmologists, contact lens technicians, and opticians. The patient base of the typical practice was made of approximately 46% contact lens wearers and the average number of contact lens fittings and refittings in a typical week was about 43.

Practitioners estimate that 61% of their patients purchase contact lenses from their practice (59% in 2024), whereas 28% purchase them online (23% in 2024), 8% purchase through a third-party retailer independent of a practice, and 4% from another practice setting.

Further to this, 54% of practitioners believe that they will see an increase in their overall contact lens practices in 2026 (vs 64% for 2025), while 46% believe it will stay the same (vs 36% for 2025).

Lens Dispensing and Mode of Wear Trends: As we have reported in years past, SiHy materials make up most of the fits and refits that are conducted today (Contact Lens Spectrum market data). For 2025, SiHy lenses were reportedly used in 66% of fits, hydrogels in 21%, GPs in 10%, and hybrids in 2% of fits.

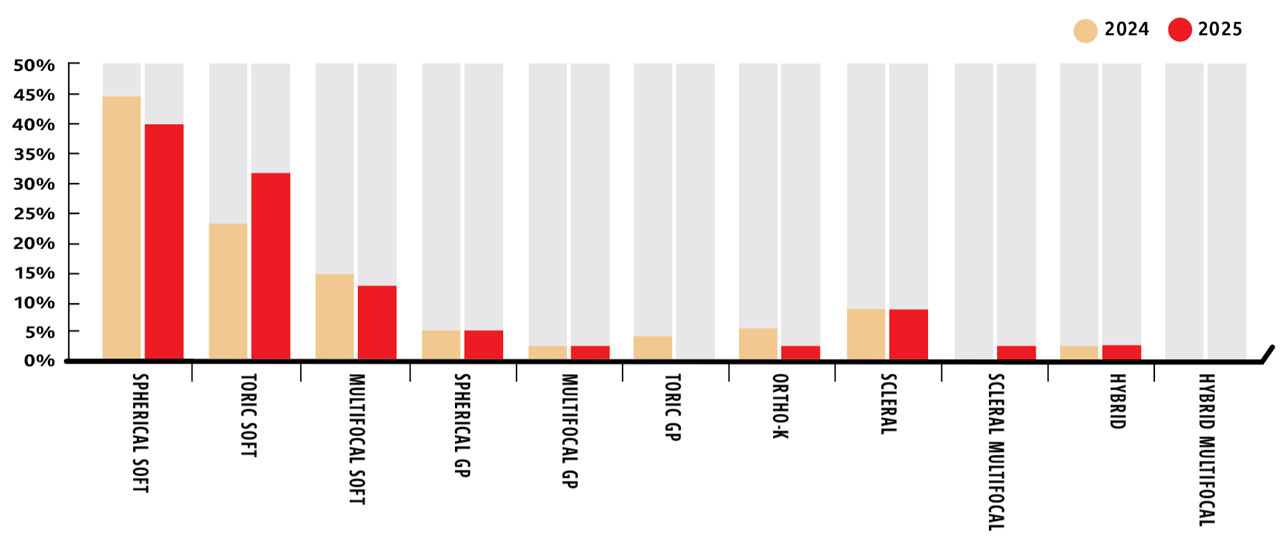

As shown in Figure 1, data from Contact Lens Spectrum’s market research showed that across all contact lens designs, most of the reported fits and refits use soft spherical lenses (41% vs 45% in 2024), followed by soft toric lenses (31% vs 24% in 2024), soft multifocal lenses (14% vs 15% in 2024), scleral designs (7% vs 7% in 2024), and spherical corneal GPs (3% vs 3% in 2024).

Along these same lines, when asked about the greatest growth potential of several popular specialty lens options in 2026, most practitioners indicated scleral lenses (58% compared to 46% for 2025), followed by custom soft lenses (23% compared to 25% for 2025), orthokeratology (ortho-k) (15% compared to 20% for 2025), and hybrids (6% compared to 9% for 2025).

When we asked practitioners to estimate the distribution of contact lenses by category of lens design for lenses containing rigid GP lens materials, it is perhaps not surprising that corneal designs made up the bulk of fits (54% vs 62% for 2024), followed by scleral lenses (26% vs 21% for 2024), ortho-k lenses (10% vs 13% for 2024), and hybrid lenses (10% vs 3% for 2024).

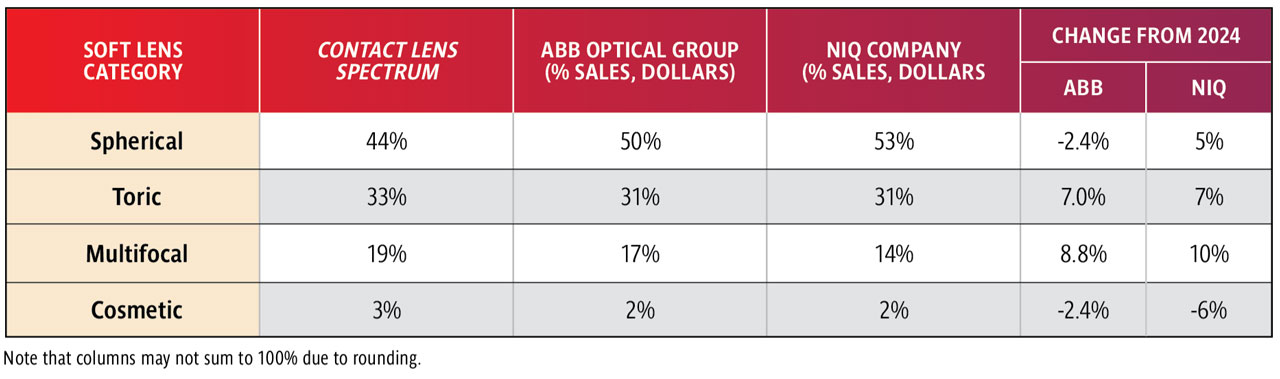

Data obtained from the ABB Optical Group (an independent optical industry platform) and NIQ (a market research service) showed a similar trend for 2025 when comparing what are considered the 4 major soft lens categories (spherical, toric, multifocal, and cosmetic) (Table 2). As expected, spherical soft lenses maintained the most market share, followed by torics, multifocals, and cosmetics.

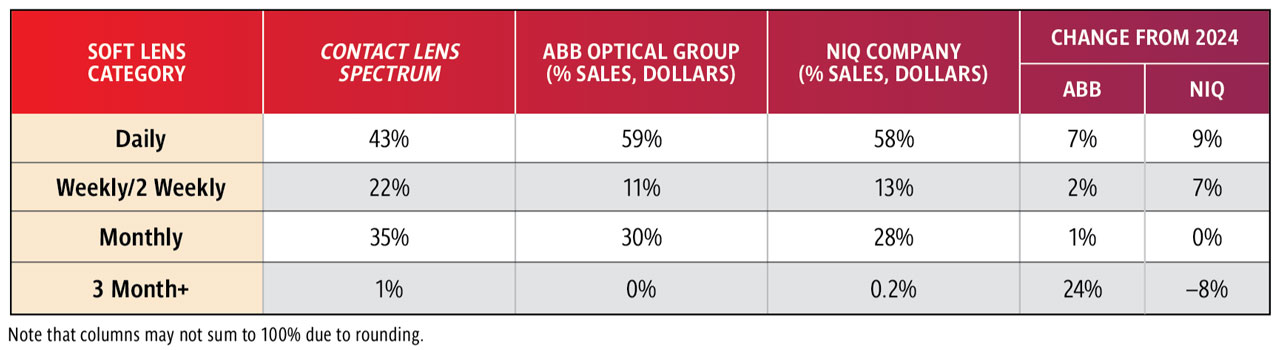

In addition to the Contact Lens Spectrum Reader Profile Survey, market insights were gleaned from ABB Optical Group and NIQ in terms of replacement schedule usage (Table 3). When comparing the data sources, stable trends emerge—for all 3 sources, the daily disposable modality continues to lead in terms of prescribing by soft lens replacement schedule (range of 43% to 59%), followed by the monthly category (range 28% to 35%).

Myopia management with contact lenses is certainly a growing practice. Yet, in 2025, 46% of Contact Lens Spectrum Reader Profile respondents indicated that they actively practice myopia management with contact lenses (compared with 59% in 2024). Of those who are practicing myopia management with contact lenses, most are using a soft multifocal (80% vs 68% in 2024) compared with ortho-k (20% vs 32% in 2024).

Yesterday, Today, and Tomorrow

Every year, we end the annual report with a look back at the contact lens industry of a decade ago. This year, as we celebrate Contact Lens Spectrum’s 40th anniversary, we will go back further to our inaugural issue in 1985. Additionally, we offer some predictions as to where we see the industry heading in the near future.

In 1986, Contact Lens Spectrum founding editor Neal J. Bailey, OD, PhD, reported that extended-wear hydrogel lenses were causing corneal ulcers. Dr. Bailey stated, “Reports of many serious corneal ulcers as a result of extended wear of soft lenses have reached us, and, as such, must be very obvious to our readers; they have also reached the wire services.” He concluded, “Only better doctor-patient-manufacturer compliance in an atmosphere in which each really cares can produce happier extended wear data.”

He also indicated that the “ulcer scare” impacted the contact lens market overall, resulting in flat sales. At the time, the size of the market was between 14 million and 19 million wearers, and soft lenses accounted for approximately 60% of all lenses in use. The GP industry was on the rise in 1985, but Dr. Bailey noted, “Analysts generally believe that the soft lens will remain as the dominant lens for at least the foreseeable future.” As seen in Figure 1, soft lenses continued to make up a majority of the lenses in use in 2025. That said, GP usage has increased substantially since 1985.

Jumping ahead to a decade ago, the 2015 Contact Lens Event of the Year was the passing of Professor Brian Holden and the profound impact that he had on the field of contact lenses since the early 1970s. Professor Holden is most known for his work in the areas of silicone hydrogel lenses and myopia research, as well as his humanitarian work in making eye care accessible globally. His study of myopia loosely ties in with this year’s Contact Lens Event of the Year, with continued advances and changes in the myopia category each year.

Looking toward the future, there are several areas in which we expect to hear news next year. Over the past few years, there have been several prototypes of and research into lenses that can monitor and diagnose various health conditions. We anticipate that early versions of intraocular pressure (IOP)-monitoring lenses will begin appearing in glaucoma specialty practices in 2026. Additionally, we believe news will be forthcoming regarding approvals for tear-based glucose biosensors that can be used in small human feasibility studies. Finally, a lens previously available for allergy patients released an antihistamine. That lens was subsequently discontinued. This year, we expect to see drug-eluting lenses gain momentum again in research and development in the areas of glaucoma or dry eye agents.

On a related note, expect to see prototypes or demos of augmented-reality contact lenses. Although we do not think that smart contact lenses will move from lab to launch in 2026, significant progress will be made.

With the US Food and Drug Administration approval of a spectacle for myopia control, potential pharmaceutical options coming to market, and continued development of contact lens options, myopia is still having its day. We predict an expansion in this category in 2026 to include adults as well as children. We think companies will begin to explore adult myopia management (especially for heavy digital-device users) with designs that target visual comfort, accommodative strain, and axial length stability.

We also predict an increase in presbyopia products, especially with a large group of Gen X and younger Boomers reaching the presbyopic age and starting to experience worsening symptoms, respectively. A number of pharmaceutical options have come on the market recently. In the coming year, expect to see contact lens manufacturers investing more heavily in new presbyopia designs, such as aspheric optical designs, improved center-near and center-distance multifocals, extended-depth-of-focus lenses, and wavefront-optimized optics that reduce halos and flares. Future technologies in this area include adjustable-focus lenses (adaptive optics), smart lenses that shift focus electronically, and combination approaches, such as using pharmaceutical therapies in conjunction with contact lenses. It won’t be surprising if presbyopia becomes the next “myopia-control-like” innovation race.

References

1. Johnson JD, Reinhardt D. Baird Equity Research. Fall 2025 contact lens survey–improved market outlook encouraging. November 11, 2025.